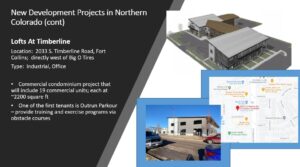

Information about new commercial projects in Northern Colorado.

Fort Collins and Northern Colorado Real Estate

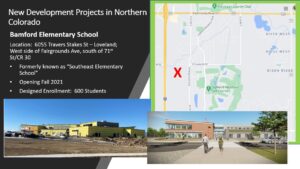

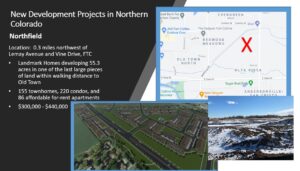

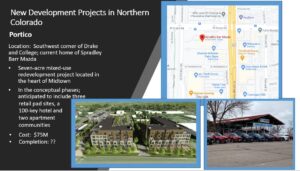

Information about new commercial projects in Northern Colorado.

The housing market frenzy from 2020 is expected to carry over into the new year. If you’re navigating the market in 2021, here are insights to help guide your journey.

Low interest rates can reduce a monthly payment by as much as $100-$200, motivating many renters to transition into homeownership.

The number of buyers entering the market coupled with low interest rates is contributing to record low inventories and high prices across the country.

As a buyer, you need to be emotionally prepared for navigating a competitive market. You will likely compete with multiple offers and may have to look for a longer time period to find the right home.

Homes in many markets are selling for well above the asking price. Buyers should be prepared to make offers on several homes before having an offer accepted. Cash buyers can be at a definite advantage.

If you are a Buyer who can pay a price above the anticipated appraisal value of the home, be sure your offer includes the terms of how an appraisal shortfall will be absorbed.

Strategies that can strengthen your offer include increasing the earnest money above the amount requested by the seller, a flexible timeline that meets the sellers’ needs, and a preapproval letter from a qualified local lender or documentation to support your cash offer.

It’s okay to have a wish list as long as you’re flexible.

After a year of social distancing, buyers are looking for space that allows family members to enjoy privacy, such as home offices and outdoor space. Some buyers are

looking for in-law suites to bring the family under one roof, either now or in the future. The trend for buyers to accommodate aging relatives has grown during the pandemic.

As a seller, you may not be able to control the square footage or floor plan of your home, or provide access to outdoor space, but there’s one thing that will help to make your

home stand out: renovations.

If buyers have a choice between an updated home and one that is not, renovated homes typically have greater appeal. In spite of reduced inventory, homes needing

work can linger on the market.

An experienced agent can help you get the house you want, the most money for a home you’re selling, and help you feel secure and confident throughout the complex process of real estate.

Give me a call to discuss your next home sale or purchase!

Source news.remax.com

A reverse mortgage allows homeowners age 62 and older to convert part of the equity in their home into cash without having to sell their home.

These loans aren’t a cure-all for retirement money problems, though. Consider these risks and benefits.

PRO: Supplemental retirement income

Some people are house-rich and cash-poor. Assuming borrowers can manage the expenses of owning a home, the reverse mortgage provides a way to liquefy a portion of the home equity to cover financial obligations. This could be helpful in the event of an unexpected job loss, health issues or limited savings. Reverse mortgages can also be a funding source to diversify investment portfolios, although loan fees add to the upfront costs.

PRO: Pay off an existing mortgage

With enough equity in the home, a reverse mortgage can be used to pay off the current mortgage, eliminating the monthly mortgage payment, and freeing up money for other

expenses.

PRO: Proceeds are tax-free

The IRS considers proceeds from a reverse mortgage to be a loan, not income, so you won’t pay taxes on it.

CON: Loan Costs

Obtaining a reverse mortgage includes loan fees, possibly mortgage insurance premiums, and interest charges, which are not tax-deductible.

CON: It’s not a good short-term option

Upfront costs for reverse mortgages are higher than other forms of borrowing, in part due to the federal mortgage insurance premiums. Alternative short-term financing options include credit cards, personal loans, and home equity loans.

CON: A default could result in losing the home

A default occurs when the borrower fails to meet the ongoing requirements of a loan, such as not paying property taxes or homeowners insurance, or failing to

certify that the home is their principal residence. This can lead to eviction and foreclosure, if unresolved.

CON: Heirs may not be able to keep the home

With a Home Equity Conversion Mortgage (HECM), which is insured by the US Federal Government, heirs have to pay either the full loan balance or 95% of the home’s appraised value, whichever is less. They can do this by paying cash, getting financing, selling the home or turning the home over to the lender to satisfy the debt.

Is a reverse mortgage worth it?

A reverse mortgage could be a good solution if:

• There is a long-term need for additional income, and benefits such as Medicare and Social Security have already been utilized.

• The need to use the equity in the home for income now outweighs the risk that family heirs may not be able to keep the home in the future.

Give one our agents a call to discuss other options such as moving to a less-expensive home, or to locate a reverse mortgage lender!

Source: NerdWallet

While you’re making New Year’s resolutions focused on health, wealth, and family, be sure to add resolutions for your home!

1. Streamline the stuff

Go room-by-room periodically clearing anything that you don’t use, wear or love and donate it to charity. After that, think twice about what you bring in.

Stash useful (but not beautiful) items such as DVDs, remotes and those kicked-off shoes in simple woven baskets. Clear your counters of everything you don’t use

on a daily basis.

2. Make it safe and sound

Check your house for radon. Test kits cost as little as $20 at your local hardware store. And, make sure carbon monoxide and fire detectors are installed on every floor with a bedroom. Clean dryer lint from the vents and ducts behind the dryer, and change HVAC furnace filters regularly. Check your house for adequate bathroom and attic vents to the outside to prevent mold. If your home was built or last remodeled before 1978, consider testing for lead paint and asbestos flooring.

3. Shrink your bills

Start by cutting your energy usage in your home:

• Switch off lights when you leave a room.

• Adjust the temperature settings on the air conditioner and furnace for times when you are not at home.

• Install LED bulbs and low-flow showerheads.

• Dry some of your clothes outside.

• Run the dishwasher or washing machine when they are full.

• Set your home computer to revert to sleep mode when not in use.

• Water your yard less and consider drought-tolerant landscaping.

• Give composting a try.

• Find a community resource for recycling.

• Seal and insulate ductwork for heating and cooling systems.

4. Get ready to entertain

Add some plants to bring in new energy and help clean the air. Freshen a room by picking a new accent color that shows up with new pillows or rugs and updates your look. Orient your furniture in conversation groups instead of facing the television.

5. Get your finances right

While you create your yearly budget, remember to allocate funds for improvement and annual maintenance of your house, and emergencies that may arise.

Now, get ready to breathe a little easier in your own home!

Source: hgtv.com, lifehack.org

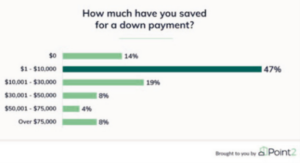

The pandemic is motivating more Millennials to feel like they’re finally ready to buy a home. But do they have the savings to do it?

Seventy-four percent of Millennials — ages 25 to 40 — recently surveyed say they are interested in purchasing a home in the next 12 months. However, 88% say they have significantly less savings than would be needed to buy a $300,000 home with a 20% down payment, or $60,000.

Fourteen percent of Millennials surveyed admit they have nothing saved for the purchase of a home.

Certainly, lower down payment programs exist. Whether these programs will be helpful for buyers whose savings are so limited is determined on a case by case basis. Down payments between 0% and 5% are possible with a home purchase, but these mortgage programs tend to cost more in the form of higher interest rates, and mortgage insurance premiums.

Forty percent of the Millennials surveyed say they set aside 10% or less of their income for a down payment. What’s more, 40% of respondents believe that $10,000 or less is enough to buy a home.

Seventy-six percent of Millennials in the study are looking for a detached home rather than a condo or townhome. Nineteen percent have their eye set on a home with more than 2,000 square feet, while 53% feel a home with 1001 – 2000 square feet will fit their needs.

If Millennial buyers are considering a down payment of 0%-5%, they may have a challenge finding homes for sale that are spacious enough to meet their demands with the amount of funds they have saved.

Those Millennials who hope to buy a home of their own may be able to save more as they move back in with their families. Young adults especially have moved in with family members as a result of the pandemic.

Call me for more information about opportunities to buy a home with a low down payment!

Source: Point2.com